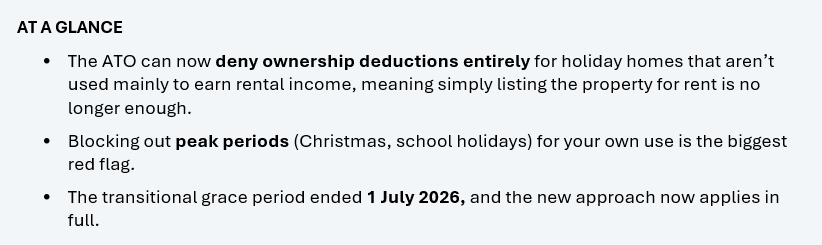

Holiday homes under new rules: what the ATO’s latest guidance means for you

New ATO rulings change the deduction landscape for holiday homes and mixed-use rental properties – and the transitional grace period has now ended.

What’s happened?

On 20 May 2026, the ATO finalised a significant package of guidance on rental property income and deductions for individual owners: TR 2026/1 (rental property income and deductions for individuals not in business), PCG 2026/2 (apportioning deductions where a property has private and rental use) and PCG 2026/3 (the ATO’s compliance approach to holiday homes that are also rented out).

Together, these replace the ruling that guided practice for decades. The guidance covers long-term rentals, short-term platforms like Airbnb and Stayz, and renting out a room in your own home, but the biggest change is for holiday homes.

For the first time, the ATO treats a holiday home that is also rented out as a potential ‘leisure facility’ under a long-standing integrity rule.

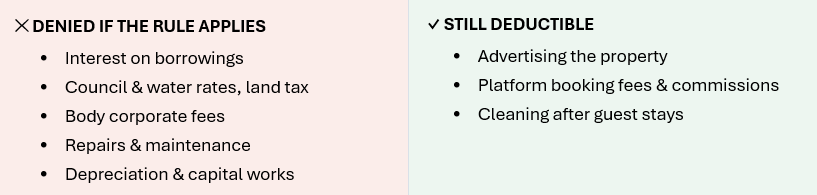

What’s at stake

Unless your property is used, or held for use, mainly to produce rental income, the ownership costs are denied altogether rather than being apportioned:

The ‘mainly’ test – peak periods matter most

Passing the test isn’t just about counting days. The ATO places particular weight on what happens in peak demand periods. A property blocked out over Christmas and school holidays for the owner’s use is at real risk, even if it’s advertised year-round.

The ATO has set out a traffic-light framework to show where you stand:

Your five-point action plan

- Review how the property is genuinely used – who stays, when, and on what terms.

- Rate yourself against the traffic lights – where does your arrangement honestly sit?

- Keep records as you go – advertising, rates charged, booking enquiries, occupancy and private use. This evidence is critical if the ATO asks.

- Don’t restructure hastily – changes made purely to sidestep the rules can trigger specific anti-avoidance provisions. Get advice first.

- Capture denied costs so they can count toward the property’s CGT cost base when you eventually sell.

We’re across the detail and ready to help

We’ve reviewed the new ruling and both compliance guidelines in detail and are already working through the implications with affected clients. Outcomes turn heavily on individual facts, meaning a review now can identify risks, confirm your deductions are claimed correctly, and make sure your records will stand up to scrutiny.

Please contact our office to discuss how the new guidance applies to your circumstances.

This article is general in nature and does not constitute personal tax advice. You should seek advice specific to your circumstances before acting on any of the matters discussed. Liability limited by a scheme approved under Professional Standards Legislation.