Federal Budget 2026–27: Decoding the reforms that will reshape tax and wealth planning

The Federal Government handed down its 2026-27 Budget on 12 May 2026, and beneath the familiar cost-of-living headlines sits one of the most ambitious tax reform agendas Australia has seen in over a decade. A rewrite of the capital gains tax (CGT) regime, the long-awaited tightening of negative gearing and a 30% minimum tax on discretionary trusts signal a meaningful shift in how individuals, families and businesses will structure their financial affairs.

In this insights piece, we unpack the measures most relevant to our clients, what they are, when they take effect, and the planning considerations they raise.

A word of caution before reading on

Most of what follows is announcement, not law. Consultation on detailed design has not yet occurred, draft legislation is yet to be released, and recent history is full of Budget proposals that were materially modified, or quietly shelved, before becoming law. The Stage 3 tax cuts, the original Division 296 design, and the various iterations of franking credit policy are all reminders that headline measures and final legislation can look very different.

- Do not make irreversible decisions on the basis of Budget night announcements. Rushing to restructure or dispose of assets before the detail is known can lock in worse outcomes than waiting.

- Use the lead time wisely. Most of the headline reforms have effective dates one to three years away. That is by design: it gives the legislative process room to run and gives advisers and clients room to plan.

- Plan strategically, not reactively. Our role over the coming months is to monitor the detail as it emerges, work through individual scenarios with clients, and act decisively when there is enough certainty to do so.

The headline reforms

Three measures stand out for their scale and the planning conversations they trigger.

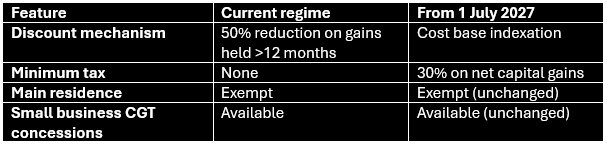

1. Capital gains tax: the end of the 50% discount

From 1 July 2027, the 50% CGT discount for assets held more than 12 months will be replaced by cost base indexation, paired with a 30% minimum tax on net capital gains. The change applies broadly, including to individuals, trusts and partnerships, and across all CGT assets including pre-1985 holdings.

The key transitional provisions:

- Gains accruing before 1 July 2027 retain the existing 50% discount.

- Pre-1985 gains that accrued before 1 July 2027 remain CGT-exempt.

- Investors in new residential properties can choose between the existing 50% discount, or the new indexation-plus-minimum-tax model.

- Age Pension and other income support recipients are exempt from the 30% minimum tax.

- The main residence exemption and the small business CGT concessions are unchanged.

Our view: Replacing a percentage discount with cost base indexation fundamentally changes the after-tax outcome on long-held assets. Whether an investor is better or worse off depends on inflation over the holding period and the size of the gain. We would be cautious about wholesale realisation strategies based on the announcement alone.

2. Negative gearing: confined to new builds

From 1 July 2027, losses from established residential investment properties will only be deductible against other residential property income, including capital gains. Excess losses can be carried forward and offset against future residential property income, but they no longer reduce salary, business or other investment income.

The budget night cut-off matters:

- The reform applies to established residential properties acquired from 7:30pm AEST on 12 May 2026.

- Properties acquired before that time, including contracts entered into but not yet settled, are grandfathered until disposal.

- Eligible new builds remain fully negatively geared.

- Properties in widely held trusts and superannuation funds are excluded.

- Targeted exemptions apply to build-to-rent developments and private investors supporting government housing programs.

Our view: Investors who exchanged contracts on or before 12 May 2026 retain access to negative gearing on those assets indefinitely. For anyone considering an established residential investment property purchase from this point on, the cashflow modelling needs to assume quarantined losses from 1 July 2027, which is a meaningfully different return profile to what investors have been used to.

3. Discretionary trusts: a 30% minimum tax

From 1 July 2028, trustees of discretionary trusts will pay a minimum 30% tax on the trust’s taxable income. Beneficiaries (other than corporate beneficiaries) will receive non-refundable credits for tax paid by the trustee.

What’s in and out:

- The minimum tax applies to discretionary trusts only.

- Carve-outs include fixed and widely held trusts (including fixed testamentary trusts), complying super funds, special disability trusts, deceased estates and charitable trusts.

- Excluded income includes primary production income, certain income relating to vulnerable minors, amounts subject to non-resident withholding tax, and income from assets of discretionary testamentary trusts existing at announcement.

- No grandfathering applies. Existing discretionary trusts are captured from 1 July 2028.

Critically, the Government has flagged expanded rollover relief for three years from 1 July 2027 to allow restructure out of discretionary trusts into companies, fixed trusts or other entity types without triggering income tax or CGT.

Our view: This is a structural reform, not a rate tweak. Family groups that have used discretionary trusts for income-streaming will need to revisit whether the rationale for the structure still holds at a 30% floor rate. The time to do that, however, is once the detail is clearer, not in the immediate aftermath of Budget night. The three-year rollover window from 1 July 2027 is the planning opportunity, and there is room for considered decisions.

An issue to watch: the bucket company double-taxation problem

Among the unresolved design questions, the treatment of corporate beneficiaries is the one that has attracted the most commentary across the profession and the financial press. As announced:

- The trustee pays 30% minimum tax on the trust’s taxable income.

- Non-corporate (individual) beneficiaries receive non-refundable credits for that trustee tax.

- Corporate beneficiaries, commonly used as “bucket companies” to cap effective rates at the corporate level, explicitly do not receive that credit.

Depending on how the legislation is ultimately drafted, the cumulative effect on income distributed through a bucket company could be:

- Trustee pays 30% on the trust’s taxable income.

- The corporate beneficiary then pays a further 30% on the distribution. This could apply either on the post-tax 70% (producing a combined corporate-level rate of around 51%), or potentially on the grossed-up amount (producing an effective corporate-level rate closer to 60%).

- When eventually paid as a dividend to the underlying individual shareholder, the total effective rate on the same income could land somewhere between 62% and 70%.

The policy intent is clear and confirmed in the Budget rationale: to discourage the use of bucket companies as an income-deferral vehicle. Treasury data indicates around 80,000 companies received discretionary trust distributions in 2022-23, with approximately 83% of those having no other business activity (in other words, operating principally as bucket companies). The reform is targeted squarely at that arrangement.

That said, several mechanical questions remain open and are subject to consultation:

- Exactly how the credit denial for corporate beneficiaries will operate, and on what base the corporate tax will apply.

- The treatment of franking credits flowing through a discretionary trust to a corporate beneficiary.

- How distributions through chains of trusts will be treated, and whether the 30% applies at each level.

- The interaction with Division 7A and existing complex trust rules.

- The scope of rollover relief for restructures, and whether stamp duty at the state level will follow the federal rollover or be triggered separately.

Our view: For clients with bucket company structures, the strategic question is not whether to act but when and how. Existing retained earnings in bucket companies and accumulated franking balances are unaffected by the reform and remain available to be paid out under the current rules. Restructuring options include winding down the discretionary trust over the rollover window, moving assets into a company or fixed trust, or repositioning the structure to focus on asset protection rather than income streaming. All of these are on the table, but the right choice will depend heavily on the final legislative design. We will be working through scenarios with affected clients as the detail emerges, and well before the 1 July 2028 commencement date.

Personal tax measures

Continuing personal tax cuts

The legislated tax cuts continue:

$1,000 instant tax deduction

From the 2026-27 income year, Australian tax residents earning income from work can claim a standard $1,000 deduction without itemising or substantiating work-related expenses. In practice:

- Taxpayers with actual work-related expenses above $1,000 retain the option to itemise in the usual way.

- Non-work deductions, including charitable gifts and professional memberships, can still be claimed on top of the standard deduction.

Working Australians Tax Offset

From 1 July 2027, a new permanent $250 Working Australians Tax Offset (WATO) will apply to income derived from work, including wages, salaries and sole-trader business income. The Government estimates this lifts the effective tax-free threshold for work income to approximately $19,985, or up to $24,985 for taxpayers eligible for the Low Income Tax Offset.

Medicare levy thresholds

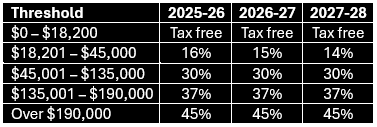

The low-income thresholds increase by 2.9% from 1 July 2025:

Small business and company measures

Permanent $20,000 instant asset write-off

From 1 July 2026 for small businesses with aggregated turnover under $10 million. Assets at or above $20,000 continue to go into the simplified depreciation pool, and the five-year lockout rule remains suspended until 30 June 2027.

Loss carry-back returns

For tax years commencing on or after 1 July 2026. Companies with aggregated annual global turnover below $1 billion can carry back a revenue tax loss and offset it against tax paid up to two years earlier, capped by the franking account balance.

Loss refundability for start-ups

From 1 July 2028. Companies with turnover under $10 million that generate a tax loss in their first two years of operation can convert that loss into a refundable tax offset, capped by FBT and PAYG withholding on Australian employees.

Monthly PAYG instalments

From 1 July 2027. Small and medium businesses can opt in to monthly reporting using ATO-approved calculations embedded in accounting software. Taxpayers with a history of non-compliance will be required to report monthly.

R&D Tax Incentive reform

From 1 July 2028: a higher core offset rate, reduced intensity threshold (2% to 1.5%), removal of eligibility for supporting R&D expenditure, increased turnover threshold of $50 million for the highest offset rate, an increased expenditure cap of $200 million, and a higher minimum expenditure threshold of $50,000.

Temporary fuel excise relief

For three months from 1 April 2026: a 60.9% reduction, approximately 32 cents per litre off petrol and diesel, with the heavy vehicle road user charge dropping to zero.

Other measures worth flagging

FBT concession for electric cars

From 1 April 2029, a permanent 25% FBT discount applies to electric cars valued up to the fuel-efficient luxury car tax threshold. Transitional arrangements preserve more generous treatment for EVs already in place:

- Electric cars valued up to $75,000 provided before 1 April 2029 retain the 100% FBT discount (0% statutory rate).

- Electric cars valued above $75,000 (up to the fuel-efficient LCT threshold) provided between 1 April 2027 and 1 April 2029 attract a 25% discount.

Private health insurance rebate

From 1 April 2027, the age-based uplift in the PHI rebate is removed. Australians aged 65 and over will receive the same base rebate percentage as those under 65.

Foreign investment in established dwellings

The temporary ban on foreign purchases of established residential dwellings is extended by two years and three months to 30 June 2029. Existing exceptions for housing-supply purchases, permanent residents and NZ citizens continue.

Foreign resident CGT regime

A time-limited concession applies to foreign investors disposing of certain renewable energy infrastructure assets, running from the first day of the next quarter after Royal Assent until 30 June 2030.

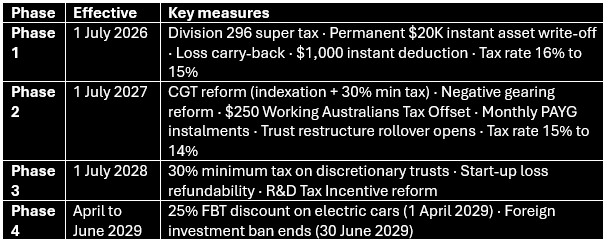

Implementation timeline at a glance

The measures take effect in waves over four years:

What this means, and what we would suggest

A few clear themes emerge from our initial review, but the overarching message is one of measured response, not urgent action.

Property investors face the biggest re-think.

The combination of negative gearing being confined to new builds and the CGT discount being replaced changes the after-tax return profile of established residential investment property meaningfully. The 7:30pm 12 May 2026 grandfathering line and the 1 July 2027 commencement date are both worth knowing about. That said, the precise after-tax outcome depends on legislation that has not been drafted yet.

Family groups using discretionary trusts have a planning window that should be used deliberately.

The three-year rollover relief from 1 July 2027 is a meaningful opportunity to assess whether the existing structure still serves its purpose at a 30% minimum tax rate, and to consider restructure options if not. The bucket company double-taxation issue in particular warrants close attention as design detail emerges. But the right strategy will only become clear once the legislation is firmer.

Small business and start-ups gain some genuine wins.

Permanent $20,000 instant asset write-off, loss carry-back, loss refundability for early-stage companies and monthly PAYG flexibility are all welcome, and warrant review of capital expenditure timing and cashflow management.

Before making any structural decision

We would encourage clients to keep three principles in mind:

- Wait for detail before acting. Restructuring decisions made on the basis of headline announcements can produce worse outcomes than the status quo if the final legislation differs from the proposal.

- Don’t dispose of assets to “beat the deadline” without modelling. The transitional provisions are deliberately generous.

- Distinguish between commercial reasons and tax reasons for holding a structure. Many discretionary trusts serve genuine asset protection and succession purposes that survive the reforms unchanged. Not every existing structure needs to be unwound.

How we’ll help

The 360Private team has been working through the Budget detail since 12 May and will continue to do so as Treasury releases consultation papers, draft legislation and final law over the coming months. Our role with clients in this period is to:

- Monitor and translate the legislative process so clients know what is actually changing, versus what has been quietly amended or dropped.

- Model individual positions under both current and proposed rules, including bucket company arrangements, property holdings, trust structures and super balances, so decisions are made on the basis of real numbers, not Budget night headlines.

- Identify the planning windows that matter most for each client’s circumstances, including the trust rollover window, the CGT transition and the Division 296 measurement dates.

- Act decisively when the time is right, coordinating with each client’s accountant, lawyer and other advisers to execute restructures, transactions and contribution strategies efficiently when the detail supports doing so.

For any clients whose structures, investments or businesses could be affected by these measures, we would welcome the conversation. The earlier modelling begins, the more options remain available. Those conversations are about preparation and analysis, not snap decisions.

The information in this article is general in nature and does not take into account any person’s individual objectives, financial situation or needs. The measures discussed are based on Federal Budget announcements as at 12 May 2026 and are subject to legislation that may differ materially from what has been announced. Clients should seek personalised professional advice from their 360Private adviser before acting on any of the information provided.